Posted on

September 11, 2018

by

Jessica Prasad

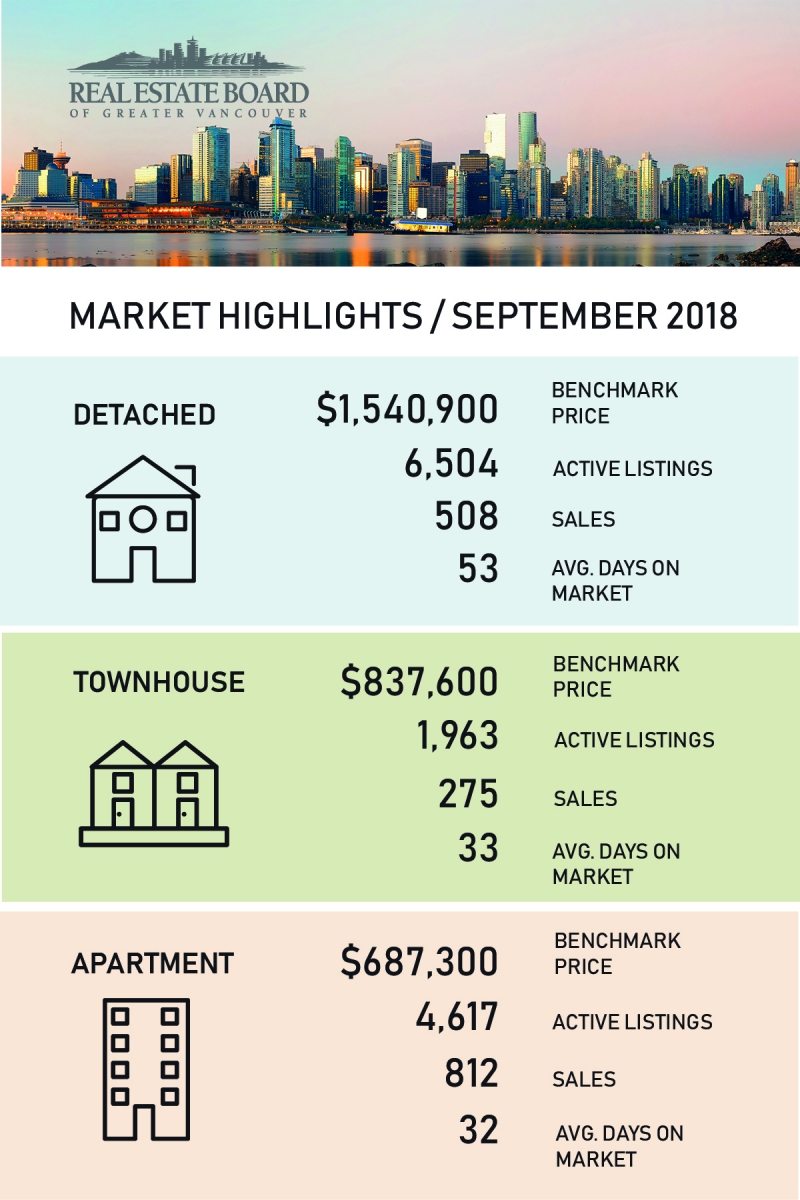

Home buyer demand stays below historical averages in August

The Metro Vancouver1 housing market continues to experience reduced demand across all housing types.

The Real Estate Board of Greater Vancouver (REBGV) reports that residential home sales in the region totalled 1,929 in August 2018, a 36.6 per cent decrease from the 3,043 sales recorded in August 2017, and a 6.8 per cent decline compared to July 2018 when 2,070 homes sold.

Last month’s sales were 25.2 per cent below the 10-year August sales average.

“Home buyers have been less active in recent months and we’re beginning to see prices edge down for all housing types as a result,” Phil Moore, REBGV president said. “Buyers today have more listings to choose from and face less competition than we’ve seen in our market in recent years.”

There were 3,881 detached, attached and apartment homes newly listed for sale on the Multiple Listing Service® (MLS®) in Metro Vancouver in August 2018. This represents an 8.6 per cent decrease compared to the 4,245 homes listed in August 2017 and an 18.6 per cent decrease compared to July 2018 when 4,770 homes were listed.

The total number of homes currently listed for sale on the MLS® system in Metro Vancouver is 11,824, a 34.3 per cent increase compared to August 2017 (8,807) and a 2.6 per cent decrease compared to July 2018 (12,137).

The sales-to-active listings ratio for August 2018 is 16.3 per cent. By housing type, the ratio is 9.2 per cent for detached homes, 19.4 per cent for townhomes, and 26.6 per cent for apartments.

Generally, analysts say that downward pressure on home prices occurs when the ratio dips below the 12 per cent mark for a sustained period, while home prices often experience upward pressure when it surpasses 20 per cent over several months.

“With fewer buyers active in the market, benchmark prices across all three housing categories have declined for two consecutive months across the region,” Moore said.

The MLS® Home Price Index2 composite benchmark price for all residential properties in Metro Vancouver is currently $1,083,400. This represents a 4.1 per cent increase over August 2017 and a 1.9 per cent decrease since May 2018.

Sales of detached properties in August 2018 reached 567, a 37.1 per cent decrease from the 901 detached sales recorded in August 2017. The benchmark price for detached properties is $1,561,000. This represents a 3.1 per cent decrease from August 2017 and a 2.8 per cent decrease since May 2018.

Sales of apartment properties reached 1,025 in August 2018, 36.5 per cent decrease compared to the 1,613 sales in August 2017. The benchmark price of an apartment property is $695,500. This represents a 10.3 per cent increase from August 2017 and a 1.6 per cent decrease since May 2018.

Attached property sales in August 2018 totalled 337, a 36.3 per cent decrease compared to the 529 sales in August 2017. The benchmark price of an attached unit is $846,100. This represents a 7.9 per cent increase from August 2017 and a 0.8 per cent decrease since May 2018.

*Editor’s Notes:

1. Areas covered by the Real Estate Board of Greater Vancouver include: Whistler, Sunshine Coast, Squamish, West Vancouver, North Vancouver, Vancouver, Burnaby, New Westminster, Richmond, Port Moody, Port Coquitlam, Coquitlam, Pitt Meadows, Maple Ridge, and South Delta.

2. A national operations team conducts an annual review of the MLS® HPI model. This review was recently completed, which resulted in some revisions to the model in August 2018. Specifically, neighbourhoods where home sales over the past three years totalled 12 or less have been removed from the model due to a lack of consistent sample size. Neighbourhoods where sales have increased to 20 or more over the past three years have been added. Historical MLS® HPI data has been recalculated to reflect these changes.

The benchmark property descriptions for what constitutes a “typical” home in a given area have also been updated to reflect changes to current buying trends.

MLS® HPI benchmark prices represent the value of a “typical” property within a market. The HPI model creates a composite description for every neighbourhood and property type based on MLS® sales data for that specific area. What people typically purchase can change over time due to changes in affordability and buyer preferences. Therefore, it’s necessary for these descriptions to be occasionally updated.

The Real Estate Board of Greater Vancouver is an association representing more than 14,000 REALTORS® and their companies. The Board provides a variety of member services, including the Multiple Listing Service®. For more information on real estate, statistics, and buying or selling a home, contact a local REALTOR® or visit www.rebgv.org.